Buy Crypto

Buy Crypto- Markets

Futures

Futures- Spot

- Copy Trade

- Earn

- More

Opinion: Bitcoin's 10-point Plunge Wasn't All Jane Street's Fault

Original Title: Notice Bitcoin selling off at market open? Jane Street is taking the blame, but the data points elsewhere

Original Author: Oluwapelumi Adejumo, CryptoSlate

Original Translation: DeepTech TechFlow

DeepTech Summary: Bitcoin recently surged to $70,000, triggering a conspiracy theory linking Jane Street to the "stock market open sell-off." This article systematically dismantles this claim from three dimensions: on-chain data, ETF structure, and options positions, concluding that the real issue is not Jane Street but the price discovery black box of the ETF era—opacity in institutional hedging that is making it increasingly challenging for retail investors to understand the market.

Full Text:

Bitcoin surged close to $70,000 in the past 24 hours, rekindling a familiar debate in the crypto market: do Wall Street institutions operating in the spot ETF ecosystem wield too much influence over price discovery?

The target this time is Jane Street—this quant trading firm is both a significant ETF market maker and a defendant in a new lawsuit related to the 2022 Terraform Labs collapse.

On social media, traders have linked Bitcoin's recent surge to a claim: alleging a mid-day price plunge pattern near the U.S. stock market open that suddenly vanished after the lawsuit was made public.

This theory spread rapidly as it blended two long-standing resonant views: distrust of large trading institutions and unease about the increasing integration of the Bitcoin market through traditional financial channels.

However, the evidence supporting the "coordinated Bitcoin suppression" scheme remains weak.

This event more evidently reveals that the structure of the spot Bitcoin ETF has made it increasingly challenging for many investors to distinguish true spot demand from market-making, hedging, and arbitrage activities.

In this sense, the Jane Street controversy transcends accusations against a single institution. At its core is how Bitcoin's new institutional infrastructure is shaping price discovery and whether the market is becoming more efficient or increasingly opaque.

Origin of the Jane Street Bitcoin Rumor

The rumor took shape after Bitcoin saw a significant rebound for two consecutive trading days. Users on X began claiming that the so-called "10 AM dump program" had vanished.

Notably, X account Negentropic, operated by Glassnode co-founders Jan Happel and Yann Allemann, played a key role in propagating this theory. They asserted: "Jane Street lawsuit being public has miraculously erased the 10 AM Bitcoin dump."

This claim quickly gained attention as Jane Street is no stranger to the scene. It is one of the world's largest trading firms and a prominent participant in the Bitcoin ETF market, serving as an authorized participant for IBIT (BlackRock's Spot Bitcoin ETF).

In practice, this positions them tightly in the core mechanism to keep the ETF share price in line with the underlying holdings' value.

Simultaneously, ongoing legal disputes involving the company further fueled the controversy.

The liquidators of Terraform Labs filed a lawsuit in Manhattan, accusing institutions including Jane Street of profiting from material non-public information related to Terraform's liquidity operations during the TerraUSD crash in May 2022.

The complaint alleges that Terraform withdrew $150 million of TerraUSD liquidity from Curve's 3pool, with wallets associated with Jane Street withdrawing around $85 million within minutes before this information became public.

Jane Street has denied any wrongdoing, labeling the lawsuit as a desperate attempt by Terraform to shift responsibility for its own actions during the loss.

This lawsuit does not prove anything about current Bitcoin trading.

However, it explains why traders quickly connected Jane Street with an observable market pattern. In the crypto world, trust is often fragile, and an institution accused in one market event often becomes a suspect in the next.

Industry Insiders Refute the Rumor

Given the above context, some Bitcoin traders believe that this top cryptocurrency has faced mechanical selling around the US stock market's open and close for months, liquidating long positions and creating liquidity vacuums in thin order books.

If this sell-off disappears after Jane Street faces new legal pressure, perhaps the firm has been pressuring the market.

Furthermore, the company's early association with FTX founder Sam Bankman-Fried has also cast a shadow over its image. Bankman-Fried worked at this trading firm before founding FTX.

This narrative is emotionally compelling but much harder to assert than to prove.

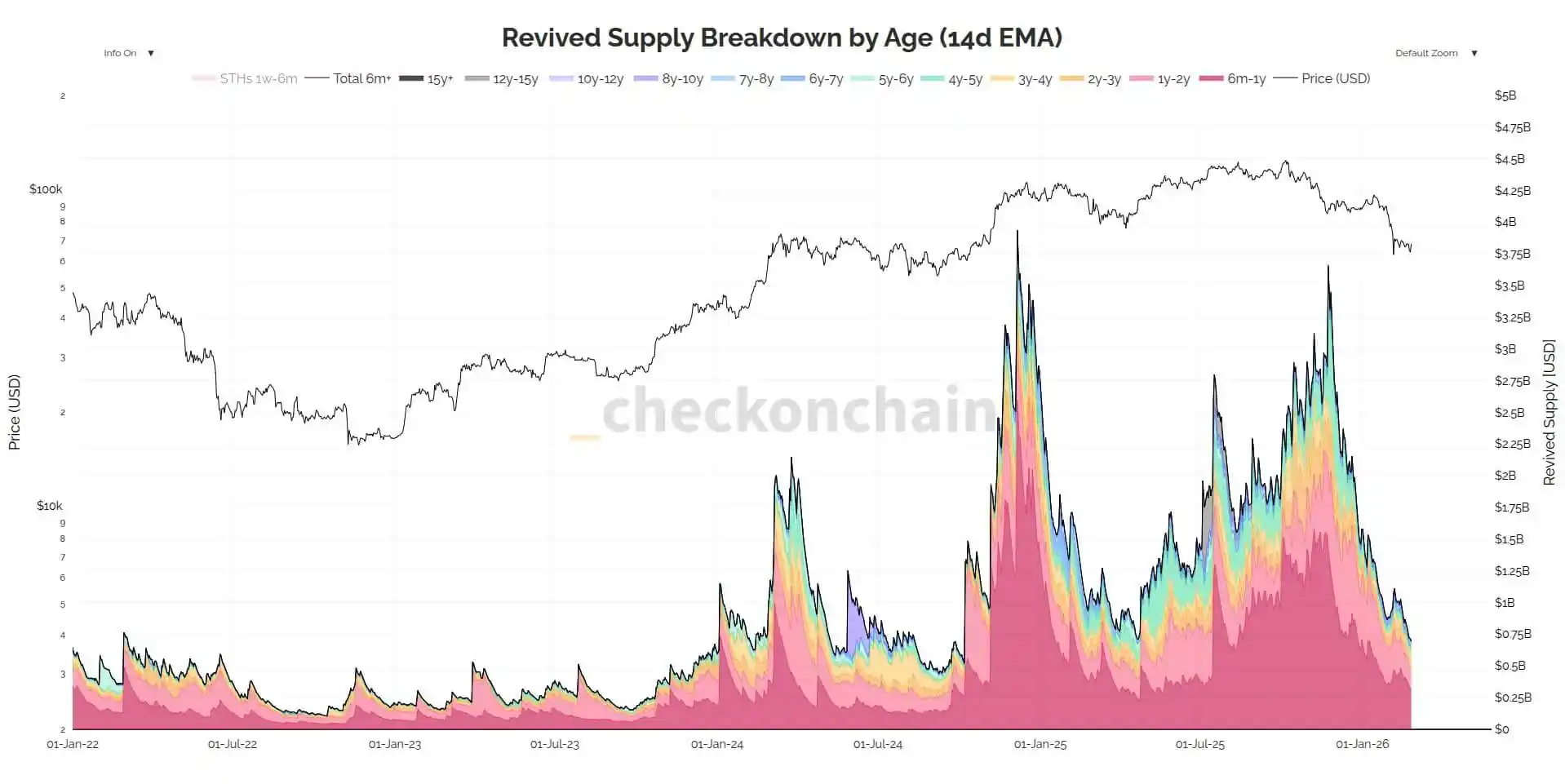

On-chain analyst James Check from Checkonchain directly refuted this argument, writing that Jane Street did not suppress Bitcoin; long-term holders selling spot drove the price action better.

Julio Moreno, Research Director at CryptoQuant, also shares a similar view, believing that this theory overlooks a more apparent driving factor: a sharp decline in Bitcoin spot demand since early October 2025.

He further added that the operational mechanism attributed to Jane Street is similar to the delta-neutral position management widely adopted by many trading firms.

The value of these rebuttals lies in their direct pointing out of the core weakness of the rumor: Bitcoin was already under broader macro repricing pressure well before entering 2026.

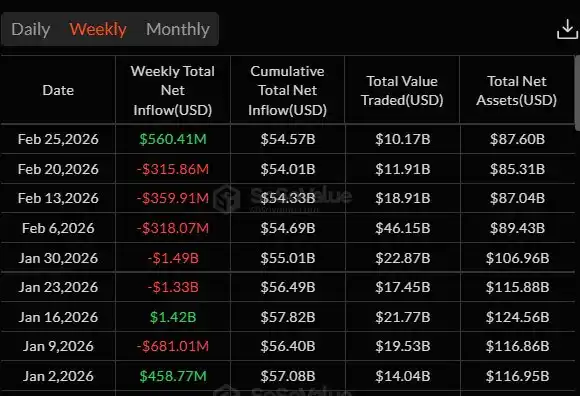

SoSo Value data shows that institutional investors have reduced Bitcoin ETF exposure for five consecutive weeks, with net outflows from spot Bitcoin ETFs totaling around $4.5 billion.

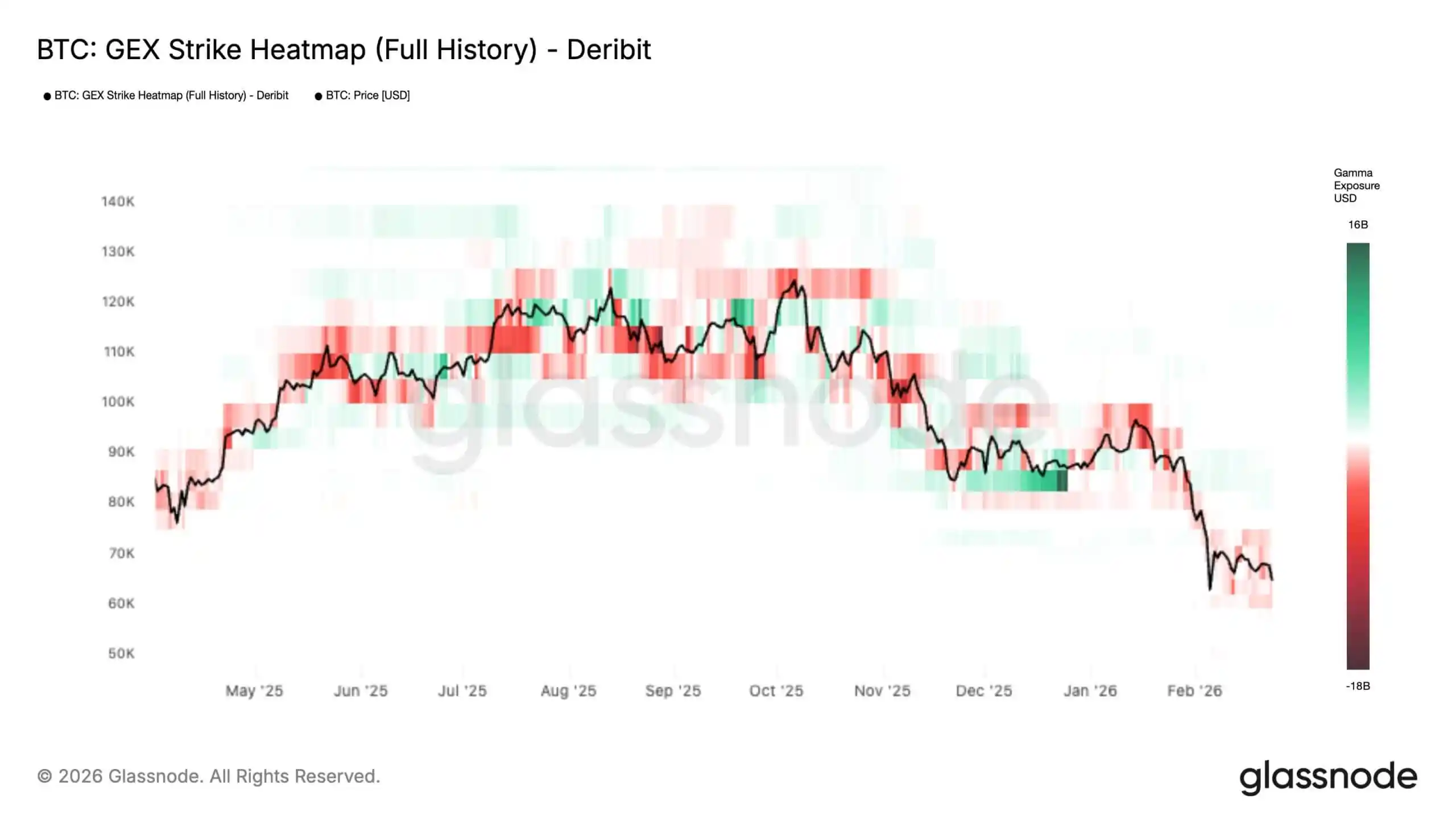

Meanwhile, Glassnode data indicates that the recurrent market pressure earlier this month has triggered a structural shift in the Bitcoin options market toward a more unstable regime.

The institution noted that the historical gamma exposure (GEX) heatmap shows that negative gamma in the current price and below region is expanding, while the positive gamma "resistance wall" above the spot price is diminishing.

In layman's terms: the options positions that typically act as shock absorbers are fading out, leaving the market more exposed to a scenario where hedging flows no longer cushion the fall but amplify it.

This dynamic is crucial: when the price is in a short-gamma range, market makers' delta hedges tend to follow the market rather than sell on the decline and buy on the rise.

The result is that the market can move faster and further on a relatively small catalyst - with larger intraday swings and a higher risk of cascading moves through key levels - until Bitcoin hits the next thick "gamma wall," at which point the hedging switches back to buffer mode.

In other words, traders are operating in an environment where "intent" is easily seen anywhere. When liquidity is thin and leverage is high, almost any sharp move can look like organized behavior.

The ETF Pipeline Is Harder to Read Than It Seems

The deeper issue raised by the Jane Street controversy is structural, not targeted at a specific institution.

As articulated by Jeff Park, Chief Investment Officer of ProCap Financial, the real issue is not whether a particular company is "exclusively suppressing" Bitcoin, but whether the ETF market structure gives authorized participants an opaque discretionary space.

This is significant because investors often rely on ETF disclosure data as a clean directional signal - but that's not the reality. While a 13F filing may show a large long ETF position, SEC guidance makes it clear that short positions are not included, and short options do not offset against long net positions.

In practice, the market may see the inventory but not the futures, options, or other hedging instruments wrapped around it.

This opacity is further compounded by the way trust is constructed. BlackRock's documentation on IBIT shows that the Trust can create and redeem shares through authorized participants and trade with designated Bitcoin counterparties.

As of that filing, these counterparties include affiliate JSCT, LLC of Jane Street Capital, and affiliate Virtu Financial Singapore of Virtu Americas.

The document also reveals that the list of authorized participants has expanded to include JPMorgan, Citadel Securities, Citigroup, Goldman Sachs, UBS, and Macquarie, among others, with more and more firms gaining access to the ETF creation/redemption mechanism.

Park's view is that this structure distorts outsiders' interpretation of ETF fund flows.

In the old cash model, creating ETF shares required the fund to buy physical Bitcoins. However, after the SEC approved the creation and redemption of crypto ETPs in July 2025, authorized participants gained greater flexibility in obtaining and delivering the underlying assets.

The SEC has stated that this change will reduce product costs and increase efficiency. However, it also means that authorized participants' exposure can be managed through a wider range of tools and counterparties, making it more difficult to determine when ETF activity reflects genuine spot demand, inventory management, basis trading, or hedging construction.

None of this is conclusive evidence of misconduct, and Park's argument does not rely on proving misconduct by Jane Street or any other company. His sharper point is this: the Bitcoin ETF era has inserted a black box between publicly available position data and the underlying price discovery process.

The initiation of a trade may look like ordinary market-making activity, as does the endpoint. What is hard to observe is the middle link: whether hedging is done through spot, futures, swaps, or some combination of the three, and whether natural arbitrage mechanisms truly transmit real spot demand to Bitcoin.

This is precisely why the Jane Street rumor struck a chord. It is less an accusation against a particular participant and more of a signal—a revelation of how limited the market's understanding of its own operational plumbing is.

Why Does the U.S. Stock Market Open Feel Like a Sell Zone?

The "10 a.m. Theory" makes sense, as even without intentional manipulation, the U.S. stock market open is naturally a period of real volatility.

This period is characterized by cross-asset rebalancing, stock-specific risk adjustments, and derivative hedging operations.

In markets where ETF intermediaries can hedge inventory with futures or other instruments, futures may pull the spot price and not just follow it.

During thin order book moments, these actions may appear larger and more conspiratorial than they actually are. Bloomberg reported earlier this month that Bitcoin market depth remains over 35% lower than October levels, highlighting how fragile liquidity has become.

Meanwhile, macro analyst Alex Kruger has stated that existing data does not support the claim of "systematic sell-off every day at 10 a.m."

He wrote that since January 1, IBIT has had a positive cumulative return of 0.9% in the 10:00–10:30 a.m. Eastern Time window, while the 10:00–10:15 a.m. window has seen a 1% decline.

In his view, this is noise, not evidence of a replicable suppression program.

Moreso, he says that the performance patterns of these two windows closely match those of the Nasdaq, indicating this is a broad-based repricing of risk assets, not a Bitcoin-specific operation.

This narrative is more in line with broader market context than a viral spread story.

If bitcoin is increasingly traded through ETF packaging as a macro risk asset, then the pressure at U.S. market open—especially in a thin liquidity market—repeatedly inducing bitcoin weakness in the same intraday window should not be surprising.

On-chain scarcity clear, price discovery not so

Bitcoin's supply is protocol-defined. No change in ETF market structure can alter this. What does change is the increasing proportion of demand—and scrutiny—that now flows through.

The Jane Street controversy unveils the gap between these two realities. On-chain scarcity is transparent, overlaid institutional plumbing less so.

Investors can see ETF circulating shares and partially disclosed holdings but cannot see every hedge, every internal net exposure, or every cross-market position that may lurk behind a market maker's book.

This blindspot creates room for misapprehension and also for distrust.

Jane Street has faced scrutiny in other markets as well, which does not help improve the situation. In July 2025, the Securities and Exchange Board of India issued an interim order relating to an index manipulation case involving Jane Street entities, with Reuters later reporting that SEBI had barred the firm from the Indian securities market during the case investigation. Jane Street also denied any wrongdoing there.

The India case is unrelated to bitcoin, but it explains why when Jane Street's name surfaced in headlines again, crypto traders were prepared to think the worst.

However, existing facts do not prove Jane Street executed a deliberate bitcoin suppression agenda.

What they prove is another thing: the post-ETF era bitcoin market has become more accessible, more institutionally integrated, and yet more inscrutable for the average investor.

You may also like

What are the noteworthy signals for the cryptocurrency industry after the Wash hearing?

High ETH BTC Price Ratio: What It Means for Traders in 2026

Explore why the eth btc price ratio just hit a 10-week high in April 2026. We analyze the massive ETH ETP inflows and what this historic pivot means for your trading strategy this year. Is Ethereum finally ready to outpace Bitcoin?

What Is the New York Lawsuit Against Coinbase? Is Your Crypto Safe After the April 2026 Case

Wondering why New York sued Coinbase and Gemini in April 2026? Here's what the lawsuit means, whether your crypto funds are safe right now, and what could change for crypto users next.

Finally, Polymarket is teaming up with Kalshi to take a bite out of this cake

ENI officially announces the completion of its strategic brand upgrade: advancing from a foundational protocol to a global institutional-level financial new infrastructure

The person who brings Web3 closest to AI

MYX Case Analysis: The Complete Harvesting Tactics Behind the Fake Surge of Cryptocurrency Tokens

Gate founder Dr. Han: The crypto winter drives structural reshaping, and everything on-chain will become a new paradigm in finance

Is XRP a Good Investment in 2026? Why Is It Stuck at $1.45

XRP is up 6.7% this week, but exchange reserves remain high. Is a volatility spike imminent? We analyze price trend, ETF inflows, whale activity, and regulatory catalysts to answer: will XRP go up, why is XRP dropping, and is XRP a good investment right now?

FC Barcelona vs Celta Vigo: Can Anyone Stop Barcelona at Home?

FC Barcelona vs Celta Vigo lineups, standings, and stats for April 22, 2026. FC Barcelona need a win to stay on track for the La Liga title. Full preview inside.

Carl Moon & WEEX Head to Mugello: The Crypto Trader's Ferrari Challenge

Forget the sidelines. WEEX is hitting the 300km/h mark at Mugello this weekend. Witness Carl Moon’s transformation from a supermarket cashier to a Ferrari racer, and discover why the world’s fastest trading floor belongs on the world’s most technical track at the official Ferrari Challenge.

How to Become a Pro Crypto Trader: WEEX Interview with Ferrari Racer Carl Moon

Ferrari racer Carl Moon on mastering crypto trading: 80/20 rule, AI tools, Bitcoin at $95K, and risk lessons from the track.

Morning Report | Amazon increases investment in Anthropic up to $25 billion; SEC plans to introduce an "innovation exemption" mechanism to support compliant on-chain trading of tokenized securities

Jeff Hoffman, founder of Booking.com: How Web3 and AI are reshaping the trillion-dollar social travel market

Top 12 Cryptocurrencies to Invest in April 2026

Key Takeaways: Bitcoin remains the dominant player with a $1.42 trillion market cap. Hyperliquid’s HYPE token gains traction,…

18 Best Crypto & Bitcoin Casinos in March 2026

Key Takeaways: Cryptocurrencies offer faster, cheaper, and more private payment options in online casinos. Top crypto casinos include…

Full Post-Mortem of the KelpDAO Incident: Why Did Aave, Which Was Not Compromised, End Up in Crisis Situation?

Key Takeaways: The KelpDAO incident exposed vulnerabilities in collateral pricing and cross-chain bridge operations, affecting Aave’s liquidity. rsETH…

Is MicroStrategy’s STRC Bitcoin’s Savior or Destroyer?

Key Takeaways: MicroStrategy’s STRC offers an annualized yield of 11.5%, driving significant Bitcoin buying pressure. Michael Saylor’s financial…

What are the noteworthy signals for the cryptocurrency industry after the Wash hearing?

High ETH BTC Price Ratio: What It Means for Traders in 2026

Explore why the eth btc price ratio just hit a 10-week high in April 2026. We analyze the massive ETH ETP inflows and what this historic pivot means for your trading strategy this year. Is Ethereum finally ready to outpace Bitcoin?

What Is the New York Lawsuit Against Coinbase? Is Your Crypto Safe After the April 2026 Case

Wondering why New York sued Coinbase and Gemini in April 2026? Here's what the lawsuit means, whether your crypto funds are safe right now, and what could change for crypto users next.