Buy Crypto

Buy Crypto- Markets

Futures

Futures- Spot

- Copy Trade

- Earn

- More

The Circle Beautiful Money Report: Is the True Winner of Stablecoins Not the Issuer?

Original Title: Circle's $461M payout shows who captures USDC yield—and it's not Circle

Original Author: Gino Matos, CryptoSlate

Original Translation: TechFlow at DeepTech

DeepTech Summary: Circle's Q4 data looks promising — USDC scale up 72% YoY, yield quintupled — but the financials reveal a harsh reality: for every $1 earned in reserve yield, $0.63 flows to gatekeeping exchanges and wallet channel providers. This article delves into the yield distribution structure, analyzing the power play between the stablecoin issuer, channel providers, and users, and how this system will come under pressure as interest rates decline.

Full Text:

Circle's Q4 report tells a growth-oriented story the company hopes investors will understand: USDC circulation grew 72% YoY to $75.3 billion, reserve yield surged 69%, and adjusted EBITDA grew fivefold.

However, the income statement presents a different picture — the issuer generates revenue only to promptly cede most of it to platforms controlling user access.

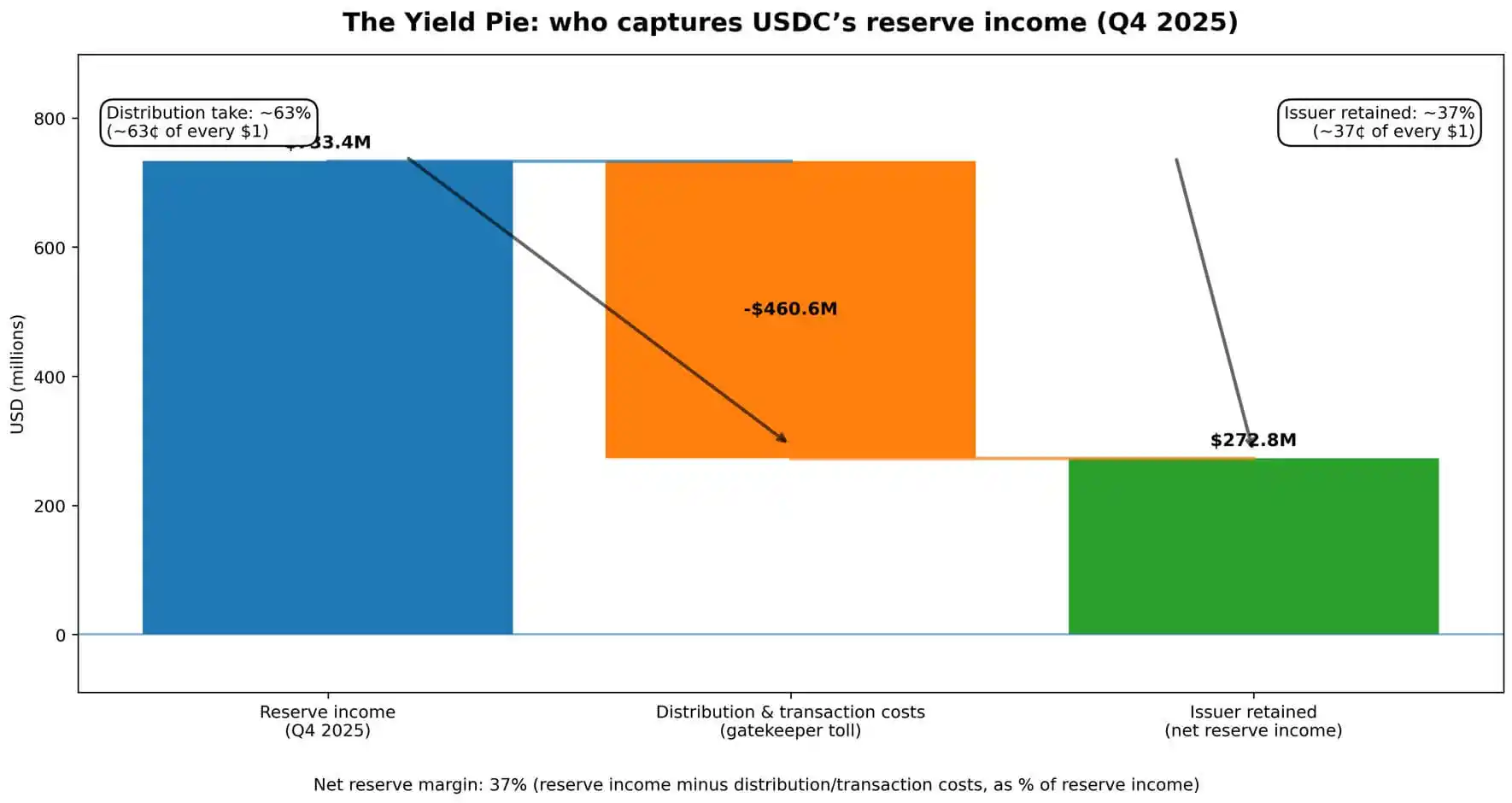

The numbers speak for themselves. Circle's quarterly reserve yield was $733.4 million.

Of this, $460.6 million was distributed and consumed as trading costs, roughly $0.63 from every $1 earned siphoned off — funds stemming from investing customer deposits.

Total revenue combined with reserve yield amounted to $770.2 million, with distribution costs representing almost 60% of all revenue flowing through the company's operations.

What Circle is left with is what remains after paying off the "gatekeepers."

This is not information hidden in the footnotes. Circle presents the "Revenue Less Distribution Costs" (RLDC) as a key performance indicator, disclosing the RLDC profit margin quarterly alongside earning data and net revenue.

The message conveyed to investors is: revenue is there, but to access it, one must pay the "shelf fee." The essence of the stablecoin business is a negotiation between the issuer and the gatekeeping exchanges, wallets, and fintech channels that effectively own the controlled balance.

Who Shares the Revenue Cake

A stablecoin generates revenue through a direct mechanism.

Users deposit dollars or convert cryptocurrency into a stablecoin. The issuer holds these funds in reserve, primarily invested in short-term government securities and similar instruments, earning the current interest rate.

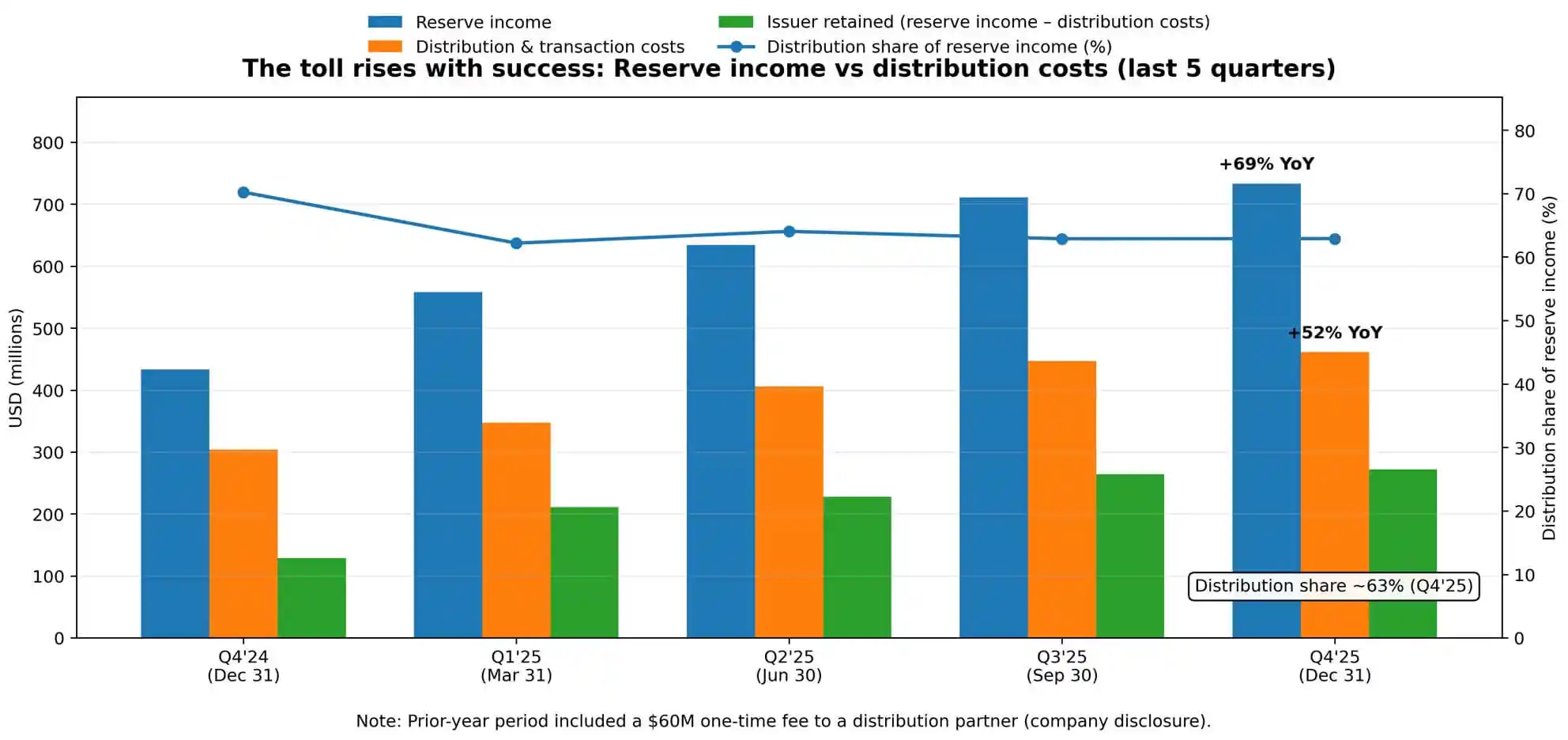

Circle's Q4 Reserve Report shows a return rate of 3.8%, down 68 basis points year-on-year, reflecting the evolution of the Fed's path. But even as interest rates decline, reserve revenue continues to climb — as the average USDC circulation doubles from $38.1 billion to $76.2 billion.

Scale outweighs rate. This dynamic is key to understanding the 52% year-on-year increase in distribution costs.

Circle explicitly attributes this growth to "increased distribution payments," noting that the prior year period included a disclosed $60 million one-time expense.

Excluding this one-time payment, the intrinsic growth of the distribution economy accelerates further. The bigger the cake, the faster the tolls rise.

Circle's net reserve profit margin — the reserve revenue minus distribution and transaction costs as a percentage of reserve revenue — remained steady at 37% in Q4.

In other words, for every $1 of total reserve revenue earned, Circle retains about $0.37, with the rest flowing to distribution partners.

This cost structure is not easily diluted as scale increases.

Distribution payments are not technology expenses, nor are they fixed costs that can be diluted with transaction volume. They are negotiated economic arrangements tied to channel positions and fund flows, meaning they are sticky and may rise further as the bargaining power of the "gatekeepers" strengthens.

Distribution "Oligopoly" Structure as Market Framework

The term "oligopoly" here is metaphorical, not accusatory. It refers to a few gatekeepers controlling user access points, extracting a proportionate share of economic benefits based on their bargaining power.

Circle's own risk disclosures make this point clear. The company warns that it may "be unable to maintain existing relationships with financial institutions and similar businesses," or establish new ones. It also highlights the risk of accepting "less favorable financial terms" and that "reliance on a few key distributors" is a structural constraint.

These terms are crucial as they position the distribution relationship as a power play rather than a vendor relationship. Circle reported a metric called "USDC on Platforms," tracking the proportion of USDC held on partner platforms to the total supply.

This figure reached $12.5 billion by year-end, a 459% year-on-year increase, with a daily weighted average representing 17.8% of total circulation. The company actively monitors where balances concentrate — once again affirming: Whoever controls the channel dictates who captures the value.

The battleground of competition is not stablecoin technology or reserve management but rather access.

Exchanges, wallets, and payment platforms sit between the issuer and the user, monetizing this position. Circle can build better products, gain regulatory clarity, and optimize reserve returns.

However, if a major distributor changes incentives or threatens to promote a competitor, the economic landscape could quickly reverse. The issuer's profit margins hinge on the terms set by gatekeepers.

What Happens in a Declining Rate Environment

Currently, this system operates in an environment with a median interest rate of around 3%, where the yield on the reserve portfolio is sufficient to support both the issuer and distributors' economic interests, leaving room for margin expansion.

But interest rates have direction, and the Fed's path is crucial. As of late February 2026, the Treasury bond yield anchoring the reserve portfolio rate remains within the 3% median range. However, the market anticipates potential rate cuts in the coming quarters.

In a declining rate environment, if distribution costs are sticky, the issuer's economic pressure will increase more rapidly than the decline in distributor cuts.

In a potential scenario, if rates fall by 100 basis points, and distribution payments remain fixed or decrease at a slower pace than reserve earnings, Circle's RLDC profit margin will face further pressure.

If rates drop another 100 basis points, under sticky distribution contracts, the issuer's economics may approach zero or even turn negative, prompting renegotiation or industry consolidation.

This is not speculation. Circle's guidance has already reflected an expected margin compression relative to a Q4 40% RLDC profit margin. The company is pricing in a world where distribution costs do not decrease proportionally to reserve earnings.

This dynamic intensifies the competition for the remaining spread, driving the entire category towards more aggressive "pay-to-play" arrangements or structural resets.

The Political Economy of Floating Reserves

A stablecoin presents an unusual political-economic arrangement.

Users provide floating reserves—$75 billion in Circle's case—but in most implementations, users do not earn a direct yield. The issuer earns the reserve yield but passes most of the share to distributors. Distributors capture economic value through control of access but do not bear asset-liability risk.

As long as users value convenience and stability over yield, this setup can function. However, once stablecoins reach mainstream scale, the question of who should receive this yield becomes increasingly hard to avoid.

The "GENIUS Act" is referenced in Circle's disclosures as legislation relevant to its regulatory environment. As the regulatory framework formalizes, the question of who should receive the yield will become harder to sidestep.

If stablecoins are serving as a deposit substitute, why shouldn't users earn interest? If they are payment rails, what justifies gatekeepers claiming such a sizeable economic share? If they are reserve assets, why can't the issuer retain a larger spread?

These are not rhetorical questions but the basis for renegotiation between issuers and distributors, platforms and users, industry and regulators in the future.

Circle's current profit margin structure reflects its bargaining power at a specific moment. This power will shift with changes in market share, regulatory posture, and alternative channels.

The Real Risk Is Not a Bank Run

Circle's balance sheet can withstand a large-scale redemption shock. The reserves are liquid, audited, and managed conservatively.

The operational risks disclosed by the company are not in the classical sense of a bank run but distributor switching—a major partner changing incentives, promoting a competitor, or building stablecoin infrastructure in-house.

This form of risk is fundamentally different from credit or liquidity risk. It is a market structure risk related to how stablecoins reach users.

If a top-tier exchange decides to prioritize support for another stablecoin, fund flows would quickly change. If a fintech platform integrates a competitor's channel, the distribution economy would reshuffle.

The issuer's options are limited: pay more to retain channel placement, accept margin compression, or build a direct-to-user distribution channel in-house—which is a capital-intensive, time-consuming alternative path.

Circle's "On-Platform USDC" metric exists because the company needs to monitor this concentration.

Where balances concentrate is where bargaining leverage resides. The more USDC is concentrated on a particular platform, the more that platform can extract in negotiations.

The issuer's profit margin is the remaining balance claim after distribution partners take their share.

Endgame Issue

The shape of stablecoin competition is akin to a bidding war for channels.

Market share capture relies not on technical or regulatory advantages but on establishing and maintaining distribution relationships.

This structure benefits issuers with capital to pay channel fees and distributors with a large enough user base to drive economies of scale.

The integration pressure is evident.

Interest rate downsides compress issuer margins. As distributors can negotiate better terms from concentrated relationships, their willingness to support multiple stablecoins decreases. Users gravitate towards defaults embedded in platforms they already use.

The entire category trends towards fewer issuers, stronger distributors, and as the revenue pie shrinks, both sides' margins are under pressure.

Circle's Q4 embodies what this logic looks like at scale.

The company generated $733 million in reserve revenue and paid $461 million to secure user access. The issuer retained $272 million leftover before deducting operational expenses.

This is the economic reality of stablecoins: they are not just digital dollars or interest rate trades.

They represent a negotiation between the issuer and gatekeepers over who captures the spread—a quarterly affair, with the stakes of this game determined by float size and rate levels.

You may also like

What are the noteworthy signals for the cryptocurrency industry after the Wash hearing?

High ETH BTC Price Ratio: What It Means for Traders in 2026

Explore why the eth btc price ratio just hit a 10-week high in April 2026. We analyze the massive ETH ETP inflows and what this historic pivot means for your trading strategy this year. Is Ethereum finally ready to outpace Bitcoin?

What Is the New York Lawsuit Against Coinbase? Is Your Crypto Safe After the April 2026 Case

Wondering why New York sued Coinbase and Gemini in April 2026? Here's what the lawsuit means, whether your crypto funds are safe right now, and what could change for crypto users next.

Finally, Polymarket is teaming up with Kalshi to take a bite out of this cake

ENI officially announces the completion of its strategic brand upgrade: advancing from a foundational protocol to a global institutional-level financial new infrastructure

The person who brings Web3 closest to AI

MYX Case Analysis: The Complete Harvesting Tactics Behind the Fake Surge of Cryptocurrency Tokens

Gate founder Dr. Han: The crypto winter drives structural reshaping, and everything on-chain will become a new paradigm in finance

Is XRP a Good Investment in 2026? Why Is It Stuck at $1.45

XRP is up 6.7% this week, but exchange reserves remain high. Is a volatility spike imminent? We analyze price trend, ETF inflows, whale activity, and regulatory catalysts to answer: will XRP go up, why is XRP dropping, and is XRP a good investment right now?

FC Barcelona vs Celta Vigo: Can Anyone Stop Barcelona at Home?

FC Barcelona vs Celta Vigo lineups, standings, and stats for April 22, 2026. FC Barcelona need a win to stay on track for the La Liga title. Full preview inside.

Carl Moon & WEEX Head to Mugello: The Crypto Trader's Ferrari Challenge

Forget the sidelines. WEEX is hitting the 300km/h mark at Mugello this weekend. Witness Carl Moon’s transformation from a supermarket cashier to a Ferrari racer, and discover why the world’s fastest trading floor belongs on the world’s most technical track at the official Ferrari Challenge.

How to Become a Pro Crypto Trader: WEEX Interview with Ferrari Racer Carl Moon

Ferrari racer Carl Moon on mastering crypto trading: 80/20 rule, AI tools, Bitcoin at $95K, and risk lessons from the track.

Morning Report | Amazon increases investment in Anthropic up to $25 billion; SEC plans to introduce an "innovation exemption" mechanism to support compliant on-chain trading of tokenized securities

Jeff Hoffman, founder of Booking.com: How Web3 and AI are reshaping the trillion-dollar social travel market

Top 12 Cryptocurrencies to Invest in April 2026

Key Takeaways: Bitcoin remains the dominant player with a $1.42 trillion market cap. Hyperliquid’s HYPE token gains traction,…

18 Best Crypto & Bitcoin Casinos in March 2026

Key Takeaways: Cryptocurrencies offer faster, cheaper, and more private payment options in online casinos. Top crypto casinos include…

Full Post-Mortem of the KelpDAO Incident: Why Did Aave, Which Was Not Compromised, End Up in Crisis Situation?

Key Takeaways: The KelpDAO incident exposed vulnerabilities in collateral pricing and cross-chain bridge operations, affecting Aave’s liquidity. rsETH…

Is MicroStrategy’s STRC Bitcoin’s Savior or Destroyer?

Key Takeaways: MicroStrategy’s STRC offers an annualized yield of 11.5%, driving significant Bitcoin buying pressure. Michael Saylor’s financial…

What are the noteworthy signals for the cryptocurrency industry after the Wash hearing?

High ETH BTC Price Ratio: What It Means for Traders in 2026

Explore why the eth btc price ratio just hit a 10-week high in April 2026. We analyze the massive ETH ETP inflows and what this historic pivot means for your trading strategy this year. Is Ethereum finally ready to outpace Bitcoin?

What Is the New York Lawsuit Against Coinbase? Is Your Crypto Safe After the April 2026 Case

Wondering why New York sued Coinbase and Gemini in April 2026? Here's what the lawsuit means, whether your crypto funds are safe right now, and what could change for crypto users next.