- Buy Crypto

- Markets

Futures

Futures- Spot

- Copy Trade

- Earn

- More

Why is it that recent acquisitions in the crypto space no longer include the token?

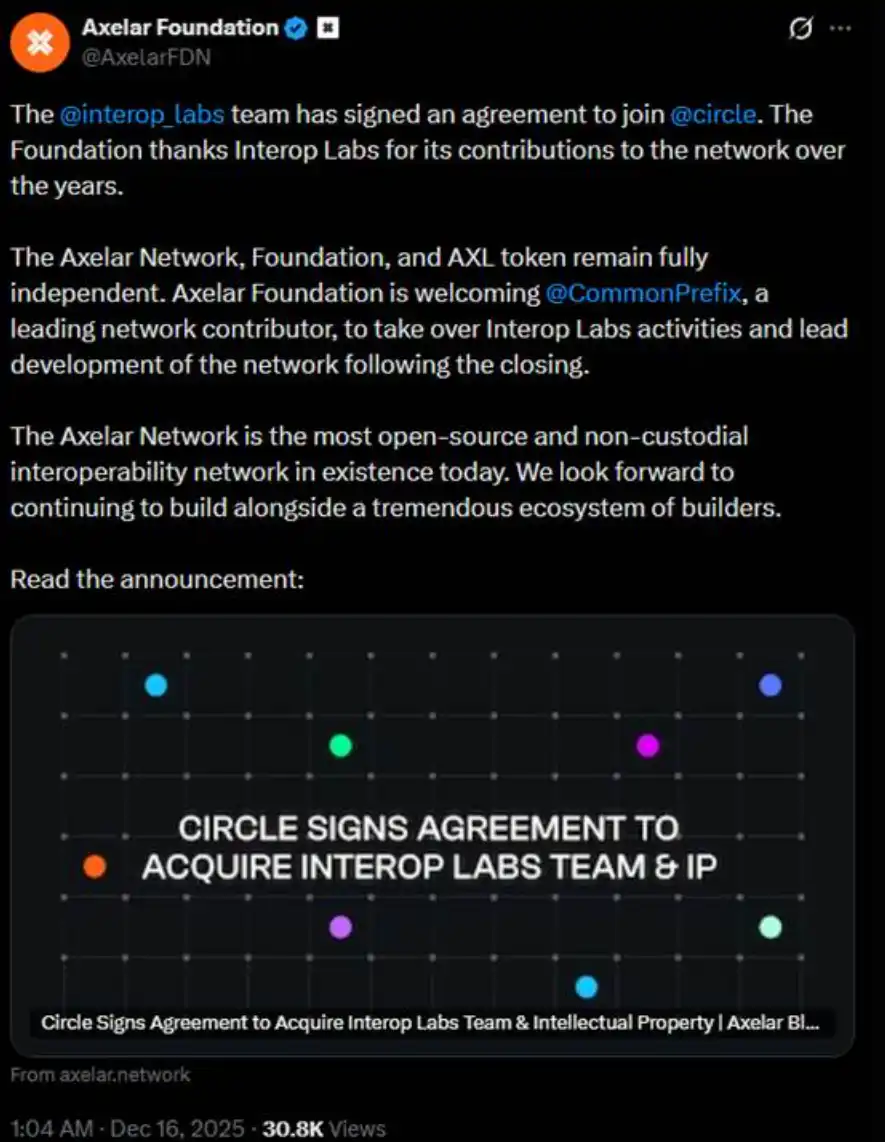

The day before yesterday, the Interop Labs team (the original developers of the Axelar Network) announced their acquisition by Circle to accelerate the development of their multi-chain infrastructure Arc and CCTP.

Normally, getting acquired is a good thing. However, the Interop Labs team's further elaboration in the same tweet caused quite a stir. They stated that the Axelar Network, foundation, and AXL token will continue to operate independently, and their development work will be taken over by CommonPrefix.

In other words, the core of this transaction is the "team joining Circle" to drive the application of USDC in the fields of privacy computing and compliant payments, rather than a full acquisition of the Axelar Network or its token ecosystem. The team and the technology are what Circle has acquired. Your original project is of no concern to Circle.

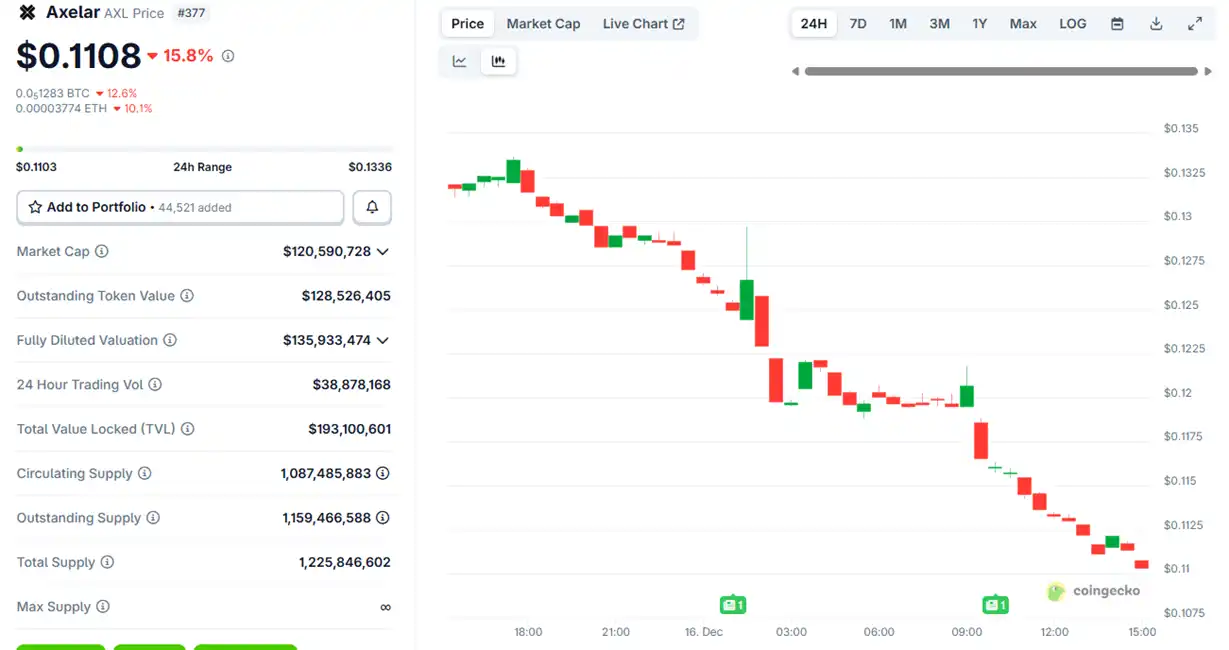

Following the announcement of the acquisition, the price of the Axelar token $AXL initially saw a slight increase before starting to decline, and it has now dropped by approximately 15%.

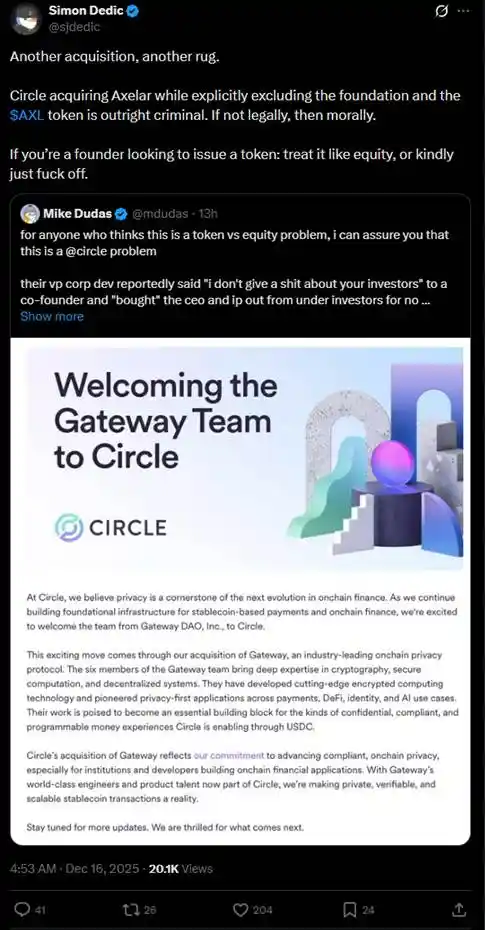

This arrangement quickly sparked a heated debate in the community about "token vs. equity." Many investors questioned whether Circle, by acquiring the team and intellectual property, effectively acquired the core assets while bypassing the rights of AXL token holders.

"If you are a founder and want to issue a token, either treat it like equity or get out."

Over the past year, similar cases of "wanting the team and the technology, but not the token" have occurred repeatedly in the crypto space, causing significant harm to retail investors.

In July, the foundation of Kraken's Layer 2 network, Ink, acquired the decentralized exchange platform Vertex Protocol based on Arbitrum, taking over its engineering team and trading technology stack, including synchronized order book, perpetual contract engine, and money market code. After the acquisition, Vertex closed its services on 9 EVM chains, and the $VRTX token was abandoned. Upon the announcement, $VRTX plummeted by over 75% on the same day, gradually approaching zero (currently valued at only $73,000).

However, holders of $VRTX still have a tiny bit of comfort because during the Ink TGE, they will receive a 1% airdrop (snapshot has ended). Next, there is something even worse: outright nullification with no compensation whatsoever.

In October, pump.fun announced the acquisition of the trading terminal Padre. Upon the announcement of the Padre acquisition, pump.fun also stated that the Padre token would no longer be used on the platform and directly expressed that there were no future plans for the token. Due to the token nullification statement in the final reply of the thread, the token instantly doubled and then sharply fell, with $PADRE currently holding only a $100,000 market cap.

In November, Coinbase announced the acquisition of Solana trading terminal Vector.fun built by Tensor Labs. Coinbase integrated Vector's technology into its DEX infrastructure, but did not involve the Tensor NFT marketplace itself or the ownership of $TNSR, with some of the Tensor Labs team transitioning to Coinbase or other projects.

The trend of $TNSR is relatively stable compared to several examples, characterized by a surge followed by a fall back, with the current price returning to a level expected of an NFT market token and still higher than the low point before the acquisition announcement.

In Web2, it is legal for small companies to be acquired by large enterprises in a "we want the team, we want the technology IP, but we don't want the equity" manner, a situation known as "acquihire." Especially in the tech industry, "acquihire" allows large enterprises to rapidly integrate talented teams and technology through this method, avoiding the lengthy process of recruiting from scratch or internal development, thereby accelerating product development, entering new markets, or enhancing competitiveness. Although disadvantageous to small shareholders, it stimulates overall economic growth and technological innovation.

Nevertheless, "acquihire" must also adhere to the principle of "acting in the best interest of the company." The reason why these examples in the crypto industry have made the community so angry is precisely because the "small shareholders" who are token holders do not agree with the project teams in the crypto industry "acting in the best interest of the company" by being acquired for the better development of the project. Project teams often dream of going public on the stock exchange when the project itself can earn big money, and then when everything is just starting or hitting a dead end, they launch a token to make money (the most typical example being OpenSea). After these project teams make money from the token, they quickly find new homes for themselves, leaving behind the past projects only in their resumes.

So, does the retail investor in the crypto space have to keep gritting their teeth and swallowing the bitter pill? It was also just the day before yesterday that Ernesto, former Chief Technology Officer of Aave Labs, released a governance proposal titled "$AAVE Alignment Phase 1: Ownership," firing a shot in the crypto community to defend token rights.

The proposal advocates for the Aave DAO and Aave token holders to explicitly hold core rights such as protocol IP, brand, equity, and revenue. Aave service provider representative Marc Zeller and others publicly endorsed the proposal, calling it "one of the most influential proposals in Aave's governance history."

In the proposal, Ernesto mentioned, "Due to some events in the past, some previous posts and comments have held strong animosity towards Aave Labs, but this proposal strives to remain neutral. The proposal does not imply that Aave Labs should not be a contributor to the DAO, or lack the legitimacy or capability of contribution, but the decision should be made by the Aave DAO."

According to crypto KOL @cmdefi's analysis, the root of this conflict lies in Aave Labs replacing the front-end integration of ParaSwap with CoW Swap, resulting in fees flowing to Aave Labs' private address thereafter. In response, Aave DAO supporters view this as a form of pillaging, as with the existence of the AAVE governance token, all benefits should primarily flow to AAVE holders or remain in the treasury to be decided by the DAO vote. Additionally, previously, ParaSwap's revenue would continue to flow into the DAO; the new CoW Swap integration changed this status quo, further convincing the DAO that this was a form of pillaging.

This starkly reflects a conflict similar to that of a "shareholders' meeting versus management," once again highlighting the awkward position of token rights in the crypto industry. In the early days of the industry, many projects promoted token "value capture" (such as earning rewards through staking or directly sharing revenue). However, starting from 2020, SEC enforcement actions (such as the lawsuits against Ripple and Telegram) forced the industry to pivot towards "utility tokens" or "governance tokens," emphasizing usage rights rather than economic rights. As a result, token holders often cannot directly share in project dividends—the project's revenue may flow to the team or VC-held equity, while token holders act as powerless stakeholders.

As seen in the examples mentioned in this article, project teams often sell team, technical resources, or equity to VCs or large corporations while also selling tokens to retail investors, ultimately resulting in resource and equity holders taking priority in profits, leaving token holders marginalized or empty-handed. This is because tokens do not have legally recognized investor rights.

In order to circumvent the regulation that "tokens cannot be securities," tokens have been designed to be increasingly "useless." By avoiding regulation, retail investors have once again found themselves in a highly passive and unprotected position. The various incidents that have occurred this year have, in a sense, reminded us that the current issue of the crypto world's "narrative failure" may not actually be that people no longer believe in narratives—narratives are still convincing, profits are still good, but what exactly can we expect when we buy a token?

You may also like

Morning News | Backpack will launch on-chain IPO subscription service; Predict.fun strategically acquires on-chain prediction platform Probable; SoFi partners with Mastercard for strategic cooperation

Inventorying the Washington power in the crypto space, who is speaking out for U.S. crypto legislation?

650 million dollars, 1.5 billion dollars, 2 billion dollars, the crypto VC landscape has changed!

Why prediction markets are the largest untapped collateral pool in DeFi

500% XAUT Staking, Zero-Fee Gold Futures and $100K Rewards: Why Traders Are Turning to WEEX for Tokenized Gold

Explore WEEX's $100,000+ gold campaign featuring 500% XAUT staking, zero-fee gold contracts, and $30,000 PAXG rewards. Trade tokenized gold today.

AI within artillery range

“The cloud” is a metaphor, but the data center isn’t.

March 4th Market Key Intelligence, How Much Did You Miss?

Taking Stock of Crypto's Washington Power Players: Who is Advocating for US Crypto Regulation?

DDC Enterprise Limited Announces 2025 Unaudited Preliminary Financial Performance: Record Revenue Achieved, Bitcoin Treasury Grows to 2183 Coins

On March 4, 2026, DDC Enterprise Limited (NYSE American: DDC) today announced preliminary, unaudited full-year financial performance for the year ended December 31, 2025. The company expects to achieve record revenue and record positive adjusted EBITDA, primarily driven by continued growth in its core consumer food business and overall margin improvement. The final audited financial report is expected to be released in mid-April 2026.

Revenue: Expected to be between $39 million and $41 million, reaching a new company high.

Organic Growth: Excluding the impact of the company's strategic contraction of its U.S. operations, core revenue is expected to grow 11% to 17% year over year.

Gross Profit Margin: Expected to be between 28% and 30%, reflecting continued operational efficiency improvements.

Adjusted EBITDA: The company expects to achieve a positive full-year result in 2025, a significant improvement from a $3.5 million loss in 2024, mainly due to rigorous cost controls and a higher-margin sales mix.

In 2025, DDC's core consumer food business maintained strong operational performance.

The company also disclosed Core Consumer Food Business Adjusted EBITDA, a metric that further excludes costs related to its Bitcoin reserve strategy and non-cash fair value adjustments related to its Bitcoin holdings from adjusted EBITDA to more accurately reflect the core business performance.

In 2025, Core Consumer Food Business Adjusted EBITDA is expected to be between $5.5 million and $6 million.

In the first half of 2025, DDC initiated a long-term Bitcoin accumulation strategy, holding Bitcoin as its primary reserve asset.

As of December 31, 2025: The company holds 1,183 BTC.

As of February 28, 2026: Holdings increased to 2,118 BTC

Today's additional purchase of 65 BTC brings the company's total holdings to 2,183 BTC

DDC Founder, Chairman, and CEO Norma Chu stated, "We are proud to have closed 2025 with record revenue and positive adjusted EBITDA, demonstrating the steady growth of the company's consumer food business and the ongoing improvement in profitability. We are building a disciplined, growth-oriented food platform and strategically allocating capital to Bitcoin assets with a long-term view, aligning with our core beliefs. We believe that this dual-track model of 'Steady Consumer Business + Strategic Bitcoin Reserve' will help DDC create lasting long-term value for shareholders."

For the full year 2025, the company defines "Adjusted EBITDA" (a non-GAAP financial measure) as: Net income / (loss) excluding the following items:· Interest expense· Taxes· Foreign exchange gains/losses· Long-lived asset impairment· Depreciation and amortization· Non-cash fair value changes related to financial instruments (including Bitcoin holdings)· Stock-based compensation

DDC Enterprise Limited (NYSE: DDC) is actively implementing its corporate Bitcoin Treasury strategy while continuing to strengthen its position as a leading global Asian food platform.

The company has established Bitcoin as a core reserve asset and is executing a prudent, long-oriented accumulation strategy. While expanding its portfolio of food brands, DDC is gradually becoming one of the public company pioneers in integrating Bitcoin into its corporate financial architecture.

Uncovering YZi Labs 229 Investment: Over 18% of the portfolio is already inactive, with an average project transparency score of 78

The business of crypto VC is becoming promising

China's AI Compute Power Counterstrike

Global Assets Plunge: Hormuz, Chips, and a South Korean Holiday

Bloomberg has reported twice, Hyperliquid once again in Wall Street's radar

Trump Backs Crypto Bill, SEC Halts Leveraged ETF, What Is the English-Speaking Crypto Community Talking About?

OpenClaw Floods Into Polymarket, Some Making Tens of Thousands Per Month

Understanding Trump's "Warfare Playbook": Ten Signals Investors Must Know

Iranian Missile Heading Toward UAE, Claude Also Within Range

Morning News | Backpack will launch on-chain IPO subscription service; Predict.fun strategically acquires on-chain prediction platform Probable; SoFi partners with Mastercard for strategic cooperation

Inventorying the Washington power in the crypto space, who is speaking out for U.S. crypto legislation?

650 million dollars, 1.5 billion dollars, 2 billion dollars, the crypto VC landscape has changed!

Why prediction markets are the largest untapped collateral pool in DeFi

500% XAUT Staking, Zero-Fee Gold Futures and $100K Rewards: Why Traders Are Turning to WEEX for Tokenized Gold

Explore WEEX's $100,000+ gold campaign featuring 500% XAUT staking, zero-fee gold contracts, and $30,000 PAXG rewards. Trade tokenized gold today.

AI within artillery range

“The cloud” is a metaphor, but the data center isn’t.