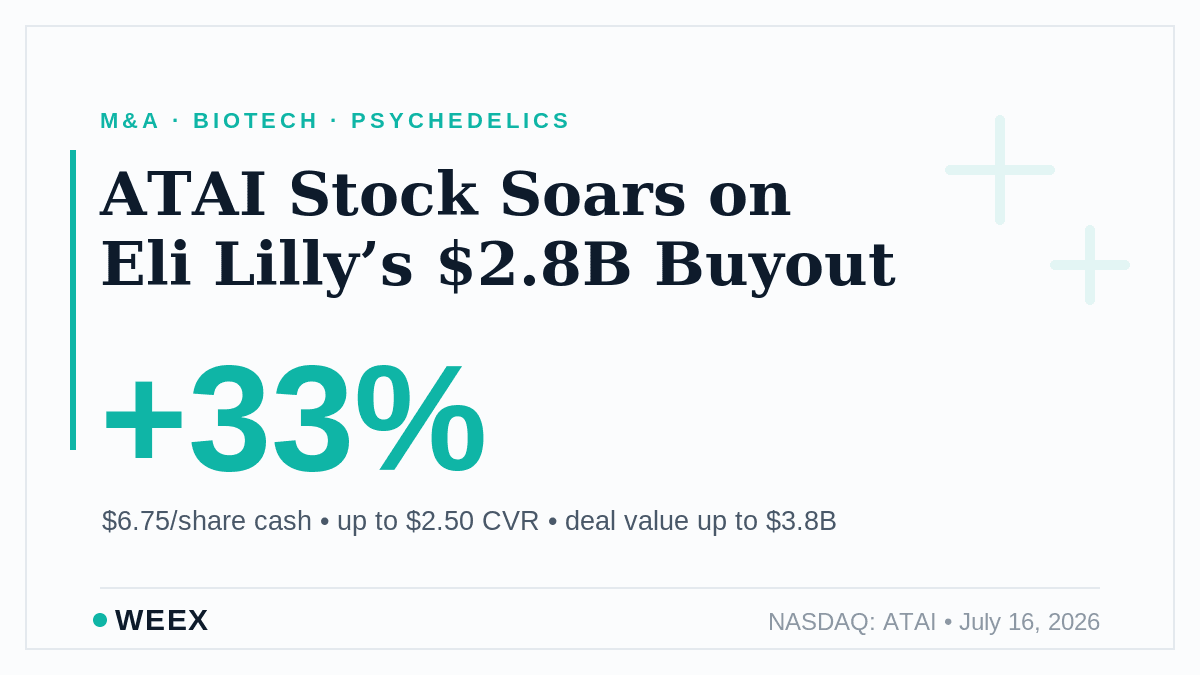

ATAI Stock Soars on Eli Lilly's $2.8B Buyout: What It Means

Prefer us on Google

Prefer us on Google

AtaiBeckley (NASDAQ: ATAI) stock jumped about 33% on July 16, 2026 after Eli Lilly agreed to buy the psychedelics drug developer for roughly $2.8 billion, or $6.75 per share in cash, plus a contingent payout worth up to $2.50 more. The move settled a long-standing question for ATAI stock holders — the market has now put a price on the company — but it changes what owning the shares is really about. This is no longer a bet on a drug pipeline. It is a bet on a deal closing and on future milestones being hit.

Here is what the deal pays, why ATAI stock is trading above the cash offer, and what the remaining upside and risk actually look like.

Why AtaiBeckley (ATAI) stock soared

The catalyst was a single announcement. On July 16, 2026, Eli Lilly said it had signed a definitive merger agreement to acquire AtaiBeckley, the clinical-stage company behind a pipeline of mental-health treatments derived from psychedelics. ATAI stock spiked as much as 32.9% to around $7.09 and touched a 52-week high near $7.08, up from a 52-week low of $2.67.

The logic is straightforward: a cash acquisition puts a firm floor under the shares. AtaiBeckley develops BPL-003 for treatment-resistant depression and alcohol use disorder, RL-007 for cognitive impairment in schizophrenia, ELE-101 for major depressive disorder, and VLS-01 for treatment-resistant depression. For Lilly, the deal adds a psychedelic-based neuroscience portfolio at a moment when the category is gaining regulatory traction. For ATAI shareholders, years of clinical-stage uncertainty were replaced overnight by a defined payout.

What the Eli Lilly–AtaiBeckley deal actually pays

The headline number is not the whole number. Shareholders receive a guaranteed cash amount at closing, plus a contingent value right (CVR) that only pays if specific milestones are met. Adding both together gets you to the "up to $3.8 billion" figure, but the two pieces carry very different levels of certainty.

| Deal component | What ATAI holders get | Certainty |

|---|---|---|

| Cash at closing | $6.75 per share | High — paid on close |

| CVR (contingent) | Up to $2.50 per share | Conditional on milestones |

| Headline equity value | ~$2.8 billion | Based on cash portion |

| Total potential value | Up to ~$3.8 billion | Only if all CVR milestones hit |

| Expected close | Q3 2026 | Subject to shareholder and regulatory approval |

The $6.75 is the part you can count on if the merger completes. The $2.50 is a maybe.

Why ATAI stock trades above the $6.75 cash offer

Notice that ATAI stock changed hands near $7.09 — above the $6.75 cash price. That gap is not a mistake. The market is assigning value to the CVR and pricing in the probability that at least some milestones pay out.

The CVR breaks down into three separate triggers, each tied to a clinical or regulatory event on a deadline:

| CVR milestone | Payout | Deadline after closing |

|---|---|---|

| Phase 3 trial of VLS-01 initiated | Up to $1.00 per share | Within 4 years |

| U.S. approval and DEA rescheduling of BPL-003 | $0.50 per share | Within 5 years |

| U.S. approval and DEA rescheduling of VLS-01 | $1.00 per share | Within 7 years |

The better way to read the current price is as merger-arbitrage math, not fundamental upside. A trader buying ATAI stock today is effectively paying about $0.34 above the guaranteed cash for a lottery ticket on drug-development milestones that could take up to seven years to resolve. Drug approvals and DEA rescheduling are far from certain, and CVRs on failed programs frequently pay nothing. The market's willingness to pay a small premium says it sees some milestone value — not that it expects the full $2.50.

Should you buy ATAI stock after the deal?

For most investors, the interesting phase of ATAI stock is over. Once a cash deal is announced, the share price detaches from the pipeline and anchors to the offer. Upside is now capped at the cash price plus whatever the CVR ultimately delivers, while downside opens up if the deal falls through and the stock re-rates back toward its pre-announcement level.

Pre-deal analyst price targets in the $14–$16 range are effectively obsolete. Those numbers assumed AtaiBeckley would remain independent and its drugs would reach the market on their own; a $6.75 cash takeout overrides that thesis. Any analyst note issued after July 16 that still carries a double-digit target is likely stale unless it is explicitly modeling the CVR. The practical decision is narrower than "is ATAI a good stock?" It is closer to "do I want to hold a capped-upside position for a small CVR premium, and am I comfortable with deal risk?"

What could still go wrong before the deal closes

A signed merger agreement is not a completed one. The deal is expected to close in the third quarter of 2026 but remains subject to AtaiBeckley stockholder approval and regulatory clearance. Several things can still move the price.

Deal-break risk is the main one: if regulators object or shareholders reject the terms, ATAI stock could fall sharply back toward pre-deal levels near the mid-single digits. Shareholder litigation is already circulating — at least one law firm has publicly said it is investigating whether the price is fair to shareholders, which is routine after buyouts but can occasionally reshape terms. And the CVR itself is the softest part of the package: each milestone depends on clinical success and DEA rescheduling within tight windows, and psychedelic-drug approvals have no guaranteed path. Treat the $2.50 as an option, not a receivable.

How crypto-native traders get stock exposure without a broker

ATAI stock is a U.S.-listed equity, so trading it directly still runs through a traditional brokerage account. That said, event-driven names like this are exactly the kind of headline traders increasingly want to react to without opening a separate broker. Some crypto exchanges have built products to bridge that gap: tokenized U.S. stocks represent shares as on-chain tokens backed 1:1 by the underlying equity, while USDT-margined products such as WEEX TradFi let users trade price moves on major stocks, indices, forex, and commodities from a single crypto account.

A caveat worth stating plainly: coverage is selective. Big, liquid names like TSLA, AAPL, and MSFT are commonly available, but a smaller biotech being taken private in an all-cash deal is unlikely to appear as a tokenized or synthetic product — and once a company is acquired, its listing disappears entirely. For ATAI specifically, the cash buyout is the trade. The broader point is that traders watching stock catalysts have more routes to market exposure than a traditional brokerage alone.

FAQ

1. Why did ATAI stock go up so much?

AtaiBeckley (ATAI) stock rose about 33% on July 16, 2026 after Eli Lilly agreed to acquire the company for $6.75 per share in cash, plus a contingent value right worth up to $2.50 per share. A cash buyout sets a firm floor under the shares, which is why the stock jumped toward the offer.

2. How much is the AtaiBeckley acquisition worth?

The cash portion values AtaiBeckley at about $2.8 billion, or $6.75 per share. Including the maximum CVR payout of $2.50 per share, the total potential value rises to roughly $3.8 billion — but the CVR only pays if specific milestones are achieved.

3. Why is ATAI stock trading above $6.75?

The market is pricing in part of the contingent value right. Buyers above $6.75 are paying a small premium for the chance that AtaiBeckley's drug programs hit clinical and regulatory milestones that trigger CVR payments over the next four to seven years.

4. When is the Eli Lilly–AtaiBeckley deal expected to close?

The deal is expected to close in the third quarter of 2026, subject to AtaiBeckley stockholder approval and regulatory clearance. Until it closes, the merger is not guaranteed.

5. Is it too late to buy ATAI stock?

After a cash-deal announcement, upside is largely capped at the offer price plus any CVR payout, while deal-break risk creates real downside. The decision is less about AtaiBeckley's pipeline and more about whether the small premium over the $6.75 cash offer is worth the merger and milestone risk.

Risk Warning

Merger-arbitrage and event-driven equity positions carry specific risks. If the Eli Lilly–AtaiBeckley deal is delayed, repriced, or terminated by regulators or shareholders, ATAI stock could fall sharply toward its pre-announcement level, and the contingent value right may ultimately pay nothing if clinical or DEA rescheduling milestones are not met. Analyst targets published before the buyout no longer reflect the cash offer. Tokenized stocks and USDT-margined TradFi products add further volatility, leverage, liquidity, custody, and counterparty risks, and are not available in all regions. Nothing here is investment advice — confirm current prices, deal terms, and product availability before acting, and never risk more than you can afford to lose.

Disclaimer: This content is provided for general branding and informational purposes only and doesn't constitute financial, investment, legal, or tax advice. Any events, rewards, online events, or related information mentioned herein should not be considered a recommendation, solicitation, or invitation to purchase, sell, trade, or otherwise deal in any crypto assets or to use any services. Crypto assets are highly volatile and may result in loss. WEEX services and online events may not be available in all regions and are subject to applicable laws, regulations, and eligibility requirements. You are responsible for ensuring that your use of WEEX services complies with local laws and for carefully assessing the risks before participating in any crypto-related activities.

You may also like

How to Buy TSMC Stock: What International Investors Need to Know Before Placing an Order

Is SPCX Stock Price a Buy Below Its IPO Price? What Happens Before August 6

SPCX Stock Price Falls Below IPO Price for the First Time: What Investors Should Do Now

TSMC Stock Price Prediction 2026-2027: Can TSM Reach $600 After the Q2 Beat?

Is TSMC Stock a Buy After Q2 Earnings? What 22x Forward Earnings and 61% AI Revenue Tell Investors

TSMC Stock Jumps After Record Q2 Earnings: What the AI Chip Boom Looks Like From the Inside

How to Buy Netflix Stock: A Guide for International Investors

NFLX Stock Price Prediction 2026-2027: Can Netflix Recover to $100?

Is NFLX Stock a Buy Before Q2 Earnings? What the 46% Decline From the High Tells Investors

FIFA World Cup 2026 Final Date: Time, Venue, and the Spain vs Argentina Showdown

NFLX Stock: What Moves Netflix and How to Trade It 24/5

ISRG Stock: Why Intuitive Surgical Fell After a Q2 Beat

TSMC Stock After Record Q2 Earnings: Why TSM Slipped

CXMT Pre-IPO Perpetual: How to Trade Hyperliquid's Chip Bet

NFLX Stock Q2 Earnings Today: What Netflix Needs to Deliver to End the 2026 Selloff

PayPal Stock Jumps 17% on Stripe and Advent's $53 Billion Takeover Bid: What Investors Should Know

Is ASML Stock a Buy After Q2 Earnings? What the €43-45 Billion Full Year Guidance Tells Investors

ASML Stock Price Prediction 2026–2027: Can ASML Reach $2,500?

ASML Stock Jumps After Q2 Beat: What the €9.3 Billion Quarter and Raised Guidance Mean for Investors

Robinhood Chain Takes Off—What Are the Key Highlights and Opportunities?

Stock Trading Platform Guide: How to Choose the Best Platform for Your Trading Style

Stock Analysis Guide: How to Read P/E Ratio, RSI, Volume, and Key Market Metrics

How to Use Grok AI for Crypto Trading: A Practical Guide for 2026

Polymarket vs. Kalshi: Which Prediction Market Platform Survives the Regulatory Crackdown?

How to Read Prediction Market Odds: A Complete Beginner's Guide

What Is Liquidity in Prediction Markets and Why Does It Matter?

How Accurate Are Prediction Markets? What the Research Actually Says

Is Polymarket Legal in the US? What the CFTC Approval Actually Means

Tokenization in Crypto vs Data Security: What Is Tokenization and How Both Protect Your Assets?